Introduction

In 2023, property owners are facing significant changes in tax implications related to rental properties. With an estimated $130 billion annually in rental income, the potential for tax deductions can mean serious savings for landlords. But many are unsure about how to maximize these deductions. This comprehensive guide aims to empower you with the knowledge needed to navigate the complexities of rental property tax deductions, integrating the implications of blockchain technology in rent collection and financial transparency.

Understanding Rental Property Tax Deductions

As a landlord, several tax-deductible expenses can help you mitigate your tax liability. Tax deductions can be broadly categorized into two groups:

- Direct Expenses: These are costs that are directly tied to the rental property. Examples include property management fees, repairs, and advertising.

- Indirect Expenses: These costs are more general and apply to the property as a whole, such as mortgage interest, property taxes, and home insurance.

1. Property Management Costs

If you hire a property management company, their fees are deductible. Services can include:

- Tenant screening

- Rent collection

- Maintenance coordination

For example, if you hire a management team at 10% of your $20,000 annual rental income, you can deduct $2,000, directly reducing taxable income.

2. Maintenance and Repairs

Expenses for necessary repairs (like fixing a leaking faucet or a broken window) can be deducted in the year they are incurred. It’s important to distinguish these from improvements, which are capitalized. For instance:

- Replacing a broken water heater is a repair.

- Upgrading to a more energy-efficient unit can be considered an improvement.

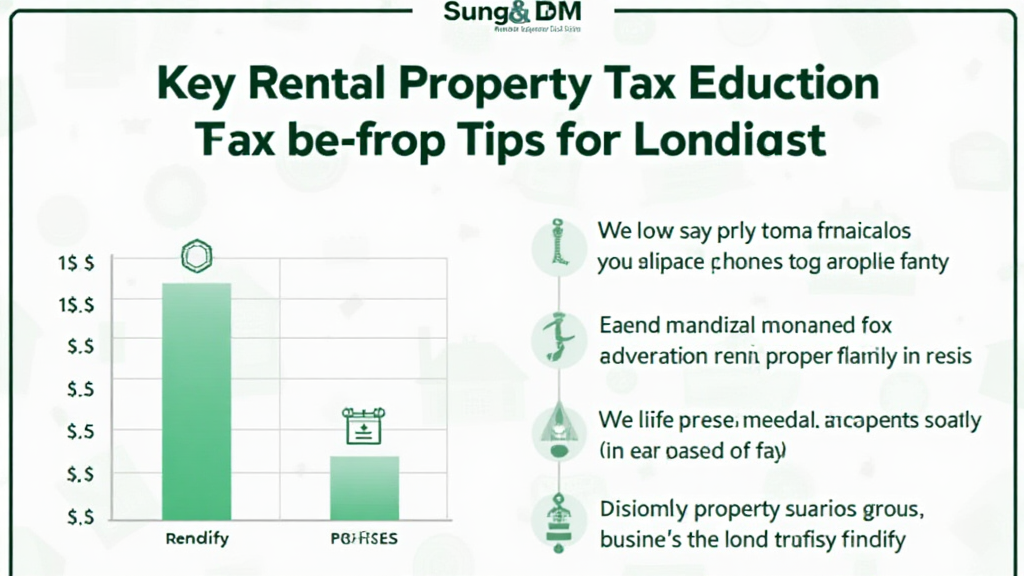

3. Mortgage Interest and Property Taxes

Mortgage interest is often a significant deduction for property owners. In 2023, the rate remains deductible as long as you meet IRS guidelines. Similarly, property taxes can be claimed, further decreasing overall tax liability. For example:

- If your mortgage interest for the year is $15,000, that entire amount can be deducted.

- Property taxes assessed at $3,000 can also be deducted, totaling $18,000 in deductions.

The Importance of Bookkeeping

Maintaining accurate records of all your income and expenses is critical. This ensures that you maximize all allowable deductions. The IRS requires detailed documentation for any deductions claimed, and rigorous bookkeeping practices can prevent costly errors.

Using Digital Tools for Bookkeeping

With advancements in accounting software, tracking your rental property profits and expenses has become easier. Tools like QuickBooks and Xero can be invaluable:

- Track income flows systematically.

- Instantly categorize expenses for tax purposes.

Blockchain and Rental Transactions

As the rental market evolves, the integration of blockchain technology offers potential benefits for landlords and tenants alike. With the application of blockchain, transactions can become more secure, transparent, and efficient. For instance:

- Using **smart contracts** for rental agreements can automate processes and ensure payments are processed promptly.

- Tenant verification can be streamlined, reducing fraud risks and enhancing trust.

This technological advancement is gradually being embraced in many markets, including Vietnam, where blockchain adoption in real estate is on the rise, demonstrated by a 45% growth in blockchain-related rental transactions in 2023.

Strategizing for Higher Deductions

To ensure you maximize your tax deductions, consider these strategic practices:

- Schedule regular property inspections to preemptively tackle potential issues.

- Invest in energy-efficient appliances and upgrades, which may qualify for additional deductions or credits.

- Keep thorough documentation of all property-related expenses, including receipts and bank statements.

Common Mistakes to Avoid

Many landlords inadvertently make errors that can affect their tax returns:

- Failing to differentiate between repairs and capital improvements can lead to misreporting.

- Not keeping comprehensive records can result in missed deductions.

Consulting with Professionals

Always consider consulting with a tax professional who understands the specific laws and regulations in your locality. Professional guidance can help ensure compliance and optimize your deductions, especially with potential changes in the tax code anticipated in 2025 that may impact rental property owners.

Conclusion

In summary, understanding and effectively leveraging rental property tax deductions can significantly impact your financial management strategy. Be proactive in maintaining accurate records, utilizing digital tools, and seeking professional advice to optimize your tax liabilities. As the landscape evolves with technologies such as blockchain, landlords in regions like Vietnam must also stay informed about the trends and adjustments that can influence their investments. Always remind yourself of your tax position throughout the year, so when it’s time to file, you can maximize your savings. By being educated in these areas, you place yourself in a position of strength in the rental property market.

For further insights and expert guidance on real estate investments and financial strategies, visit bitcryptodeposit.